Export restrictions from traditional suppliers, declining availability from established regions, and rising demand for clean energy have made Bauxite a structural theme. Guinea, with its vast reserves, has emerged as the most reliable source of bauxite amid accelerating demand for aluminium in infrastructure, electric vehicles, and renewable energy.

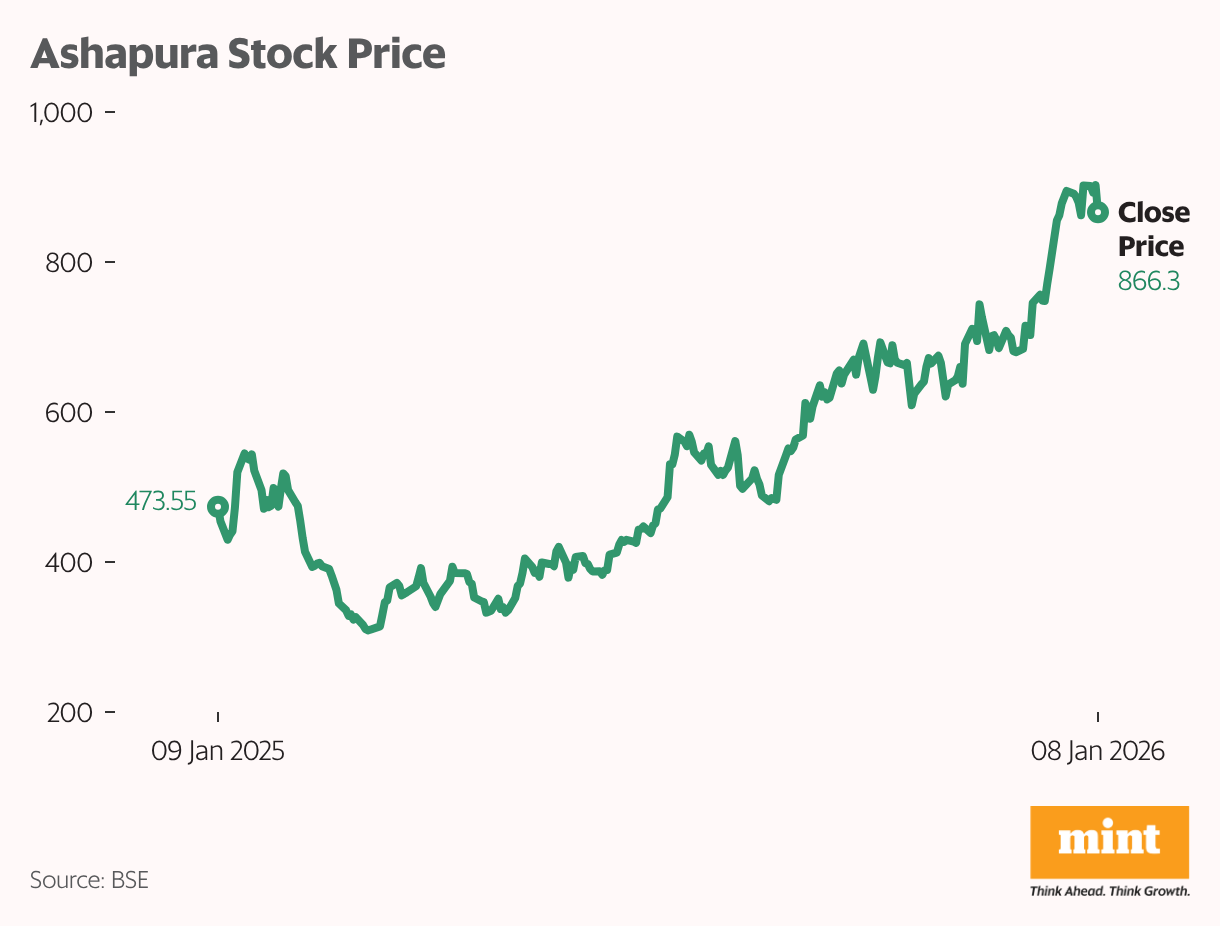

India’s aluminium demand alone is expected to more than triple by the end of the decade, underscoring the scale of the opportunity. In this changing global environment, where access to bauxite is crucial for the clean energy transition, Ashapura Minechem has formulated its growth strategy. Its share price has risen by around 100% over the last six months and by 89% over the last year. So, what’s behind the surge, and is this sustainable? Let’s take a look:

A diversified mineral platform

Ashapura Minechem has built a diversified mineral platform spanning mining, manufacturing, and trading. Established in 1982 as a bentonite-focused company, Ashapura has gradually expanded its portfolio to include bauxite, kaolin, bleaching clay, silica, and iron ore. This position is that of an integrated supplier of industrial minerals.

The company operates on a business-to-business model and caters to large customers across sectors, including fibreglass, paints, cement, civil engineering, oil and gas, and edible oil refining. Its product mix spans bentonite, bleaching clay, kaolin, and Bauxite. This allows Ashapura to address both volume-driven and value-added applications.

Bentonite anchors the domestic business

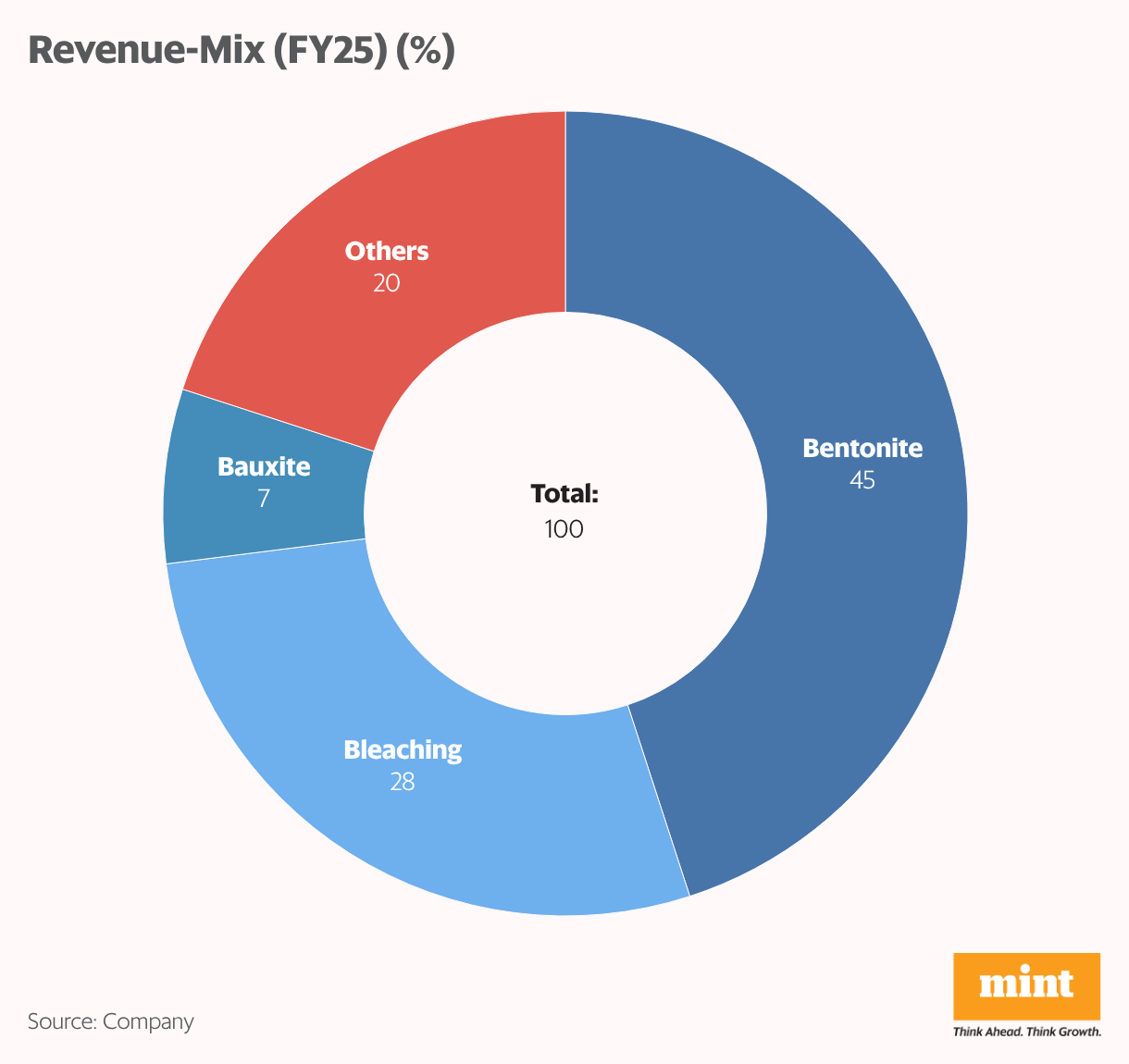

The company has a presence in India and Guinea. In India, Ashapura’s operations are diversified across multiple mineral verticals. Bentonite and allied minerals are the core of the business, contributing 45.2% of FY25 turnover. The segment serves applications in iron ore pelletizing, construction, foundry, and the oil and gas industry.

Bentonite remains the core of the company’s domestic operations, supported by high-value end-use segments and long-standing customer relationships. To strengthen competitiveness, Ashapura has recently commenced production at two new bentonite mines in Kutch. These mines are expected to support annual dispatches of around 300,000 tonnes. This will help Ashapura optimize sourcing costs and improve supply reliability for domestic customers.

Bleaching clay is the second-largest segment, accounting for 28.3% of turnover. Demand is largely driven by the edible oil refining industry. Ashapura holds a dominant 70% market share in India’s premium bleaching clay segment. This capacity is also running at peak utilization, and management is evaluating debottlenecking and brownfield expansion options to support incremental volumes.

Kaolin contributes approximately 9% to turnover and continues to see strong export demand, particularly from the fibreglass and paint industries. The Paddhar kaolin plant is operating near peak capacity, driven by overseas demand and limited spare capacity in the near term.

Bauxite as the volume engine beyond India

Although bauxite accounts for just over 7% of consolidated turnover, it is a critical volume driver for Ashapura’s international operations. This business is largely anchored in Guinea, which has emerged as the company’s most important growth geography. Note that bauxite is the primary raw material used to produce aluminium, and demand for which is growing as the clean energy transition advances.

Why Guinea sits at the centre of Ashapura’s global growth strategy

Guinea holds the world’s largest bauxite reserves, estimated at 30 to 50 billion tonnes. With the support of the Guinean government, where mining accounts for 40% of the GDP, it has become the key global destination for bauxite. Ashapura has leveraged this advantage to build a fully integrated operating model in the region.

Ashapura operates three captive ports, GSM, BOFFA, and Konta, with a handling capacity of 16 million metric tonnes (MMT). It has end-to-end control over the supply chain, with captive ports and an internal transport system. The company also manages an in-house road network exceeding 370 km, connecting mines to ports.

It has also completed a 100-meter bridge to access large, high-quality bauxite deposits in the BOFFA region. It has a long-term strategic arrangement with China Railway to strengthen its operations in Guinea. The partnership focuses on mining, transportation, and marine logistics, and aims to build a strong base to meet its large export volumes.

On a positive note, China is also the primary destination for Ashapura’s bauxite exports. This is because domestic bauxite availability in China is decreasing due to falling reserves and stricter environmental regulations. Thus, to meet domestic demand, China is currently importing about 200 million tonnes of bauxite annually, with imports increasing by 10-15% each year.

China’s clean energy transition is driving this demand. Aluminium is gaining wider adoption in carbon-reduction initiatives, particularly for the manufacturing of electric vehicles (EVs), solar energy projects, and grid expansion.

Many Chinese aluminium smelter owners are not fully integrated (meaning they don’t own their own mines), making a mine owner like Ashapura a key strategic supplier. Furthermore, with Indonesia’s export ban and Australia’s reduction in export volumes, China’s traditional bauxite sources are drying up.

Numbers have started reflecting the scale-up. In H1FY26, the company exported 3.38 MMT of bauxite, almost equal to last year’s (FY25) volume (3 MMT). In fact, bauxite exports doubled to 1.33 MMT in Q2FY26 from the same time last year. Most Bauxite sales to China are conducted on a CIF (Cost, Insurance, and Freight) basis, under which Ashapura bears all costs until the cargo reaches the destination port in China.

CIF transactions result in higher revenue because the price includes ocean freight and insurance costs. While certain customers also prefer FOB (Free on Board) arrangements, under which Ashapura delivers the mineral to the port in Guinea. Once the goods are on board, the responsibility shifts to the buyer. FOB contracts result in lower revenue because they are priced without the freight.

As demand increases with the shift towards cleaner energy, Ashapura plans to scale exports to 15 MMT by FY28. To support this growth, it is expanding capacity at its BOFFA and GSM ports. Total port handling capacity is expected to increase from 16 MMT to 27 MMT by Q2FY27. This will enable it to manage higher captive volumes and third-party cargo more efficiently.

Management describes its growth trajectory as a “linear progression,” meaning they are intentionally ramping up volumes rather than aiming to hit maximum capacity immediately. Guinea bauxite export Ebitda stood at $8.9 per metric tonnes in the first half of FY26.

Portfolio diversification within Guinea

Beyond bauxite, Ashapura is diversifying its Guinea portfolio by entering the iron ore market. It has signed a long-term sale-and-purchase contract with a local beneficiation plant. Trial production was expected to begin in late 2025. Management expects to commercialize around 1 million tonnes or more within the next one to two quarters.

Iron ore sales are structured on an ex-works basis, meaning the transaction excludes costs such as road transport, port handling, and ocean freight. Management expects ex-mines costs to be less than $10 per tonne, a fraction of the price of minerals delivered to China. It’s because logistics account for the largest share of total costs in Guinea’s mining operations.

Thus, selling ex-mines results in a relatively lower top-line than selling bauxite on a CIF basis. But lower logistics costs are expected to support good contribution margins, making iron ore an incremental contributor to profitability. Ashapura’s financial growth is also increasing rapidly due to higher bauxite export volumes from Guinea.

Performance tracking the volume scale-up

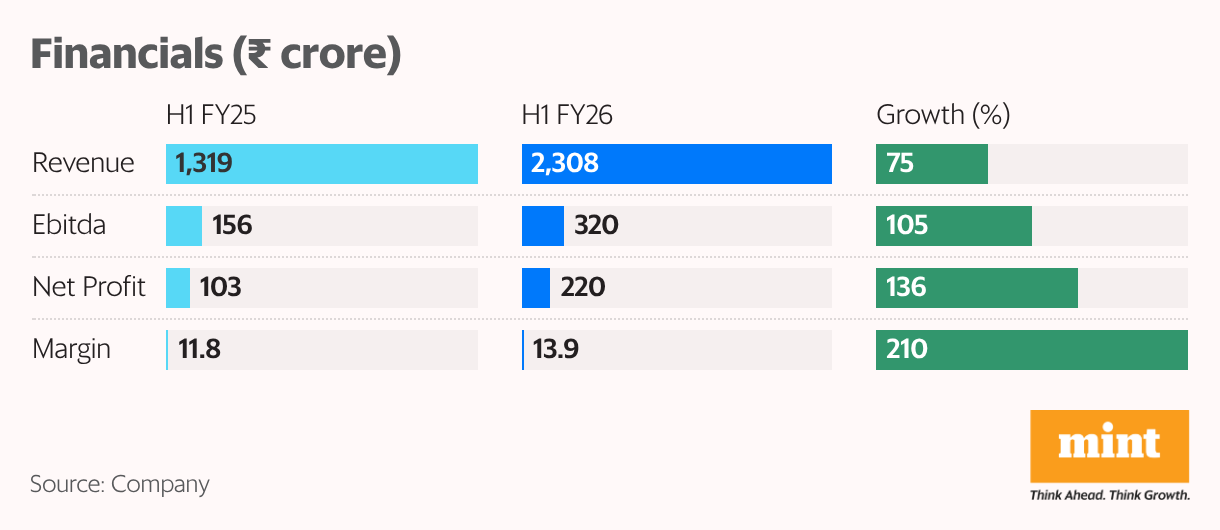

Revenue in the first half of FY26 rose by 75% year-on-year to ₹2,308 crore, while Ebitda rose by 105% to ₹320 crore. Ebitda margin also expanded by 2.1 percentage points to 13.9%. Net profit also jumped by 136% to ₹220 crore, from ₹103 crore in H1 FY25. India’s business grew by over 25% in the H1 of FY26. The company expects the second half to be even stronger.

The company is trading at an EV/EBITDA multiple of 15, above its 5-year median of 11. However, this premium could moderate as revenue growth scales into higher EBITDA. Key risks include volatility in bauxite prices and the company’s high dependence on Guinea for bauxite exports.

For more such analysis, read Profit Pulse.

Madhvendra has over seven years of experience in equity markets and writes detailed research articles on listed Indian companies, sectoral trends, and macroeconomic developments.

The writer does not hold the stocks discussed in this article.

The purpose of this article is only to share interesting charts, data points, and thought-provoking opinions. It is NOT a recommendation. If you wish to consider an investment, you are strongly advised to consult your advisor. This article is strictly for educational purposes only.

Source link

Leave A Comment