Dividend-paying companies do not attract the same attention in such phases. They tend to be ignored when growth stories dominate the narrative. Yet, dividends do something important. They put cash in the investor’s hands, reducing the need to time market cycles.

The quality of a dividend matters. It needs to come from operating cash flows, not from borrowing or one-off gains. Businesses that generate cash steadily and keep leverage under control are better placed to sustain payouts through ups and downs.

These are not stocks that promise excitement. What they offer instead is a degree of predictability. Over a three-year period, regular dividends combined with reasonable valuations can do more of the heavy lifting than is often acknowledged.

The following five stocks fall into that category.

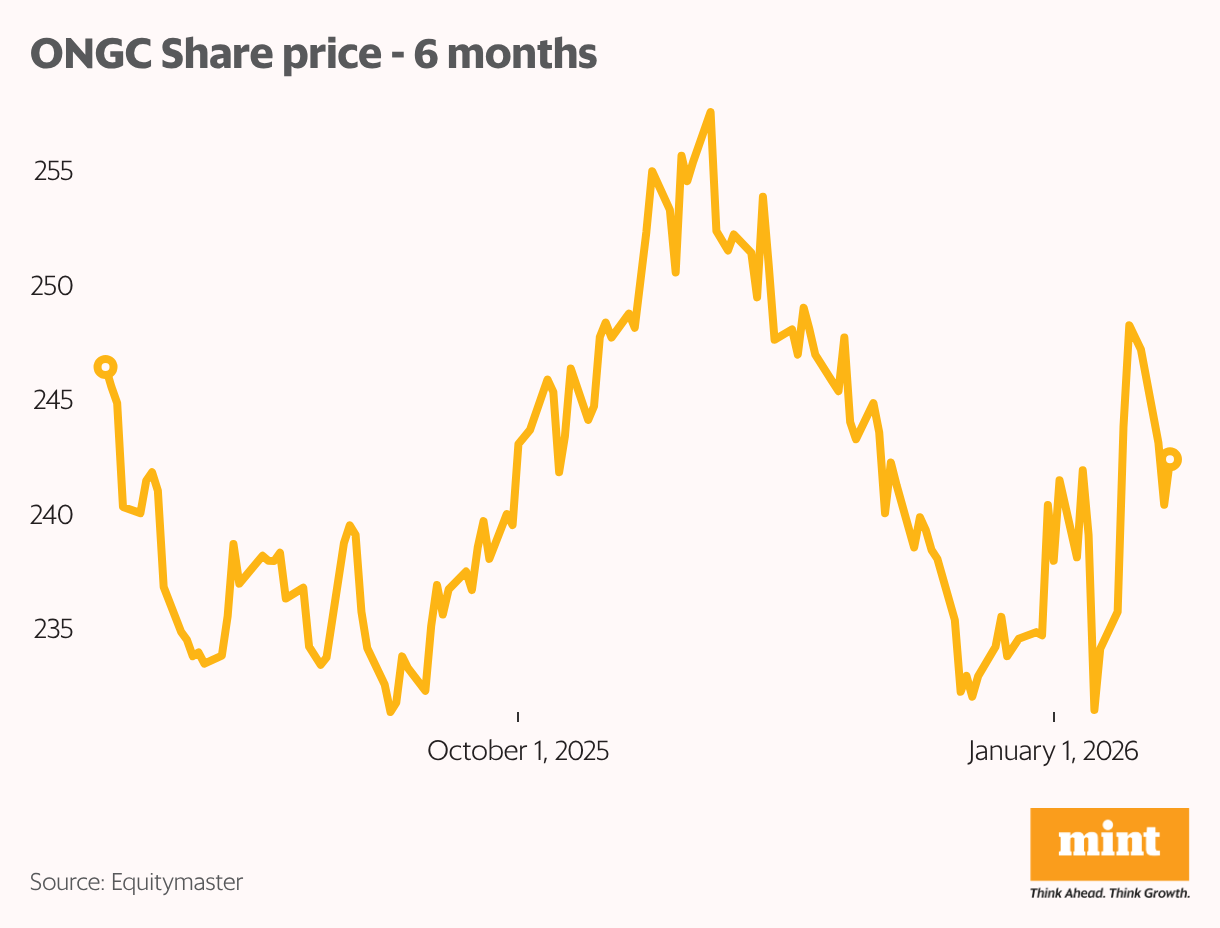

#1 ONGC

Oil and Natural Gas Corporation produces crude oil and natural gas and sits at the centre of India’s upstream energy ecosystem. It is a business where decisions taken today often show up in the numbers years later. That long cycle has also enabled ONGC to generate steady cash flows.

This consistency explains why the stock features among dividend stocks to watch over the next three years. Even when growth has slowed, ONGC has continued to return cash to shareholders, largely supported by operating cash flows rather than balance-sheet stretch.

The recent quarter was marked by familiar pressures. In Q2FY26, standalone sales declined by about 0.9% year-on-year as realised prices for crude and value-added products softened. Ebitda margins, however, held up, helped by lower recouped costs and tighter cost control.

Management expects the next phase of growth to come from gas. Production from the KG-98/2 field is expected to start rising from FY27, while additional volumes from the Daman offshore project are also scheduled to come on stream during the year. Over time, this should increase the share of higher-priced new well gas in the production mix.

Looking ahead, ONGC plans to sustain upstream capital expenditure of around ₹30000–35000 crore annually. Most of this spending is expected to be funded through internal accruals. The focus remains on new field development and gas infrastructure, while gradually slowing decline from mature fields.

At current levels, the stock trades at around 9.55 times earnings, below its long-term median valuation. Dividend yield stands near 5.04%.

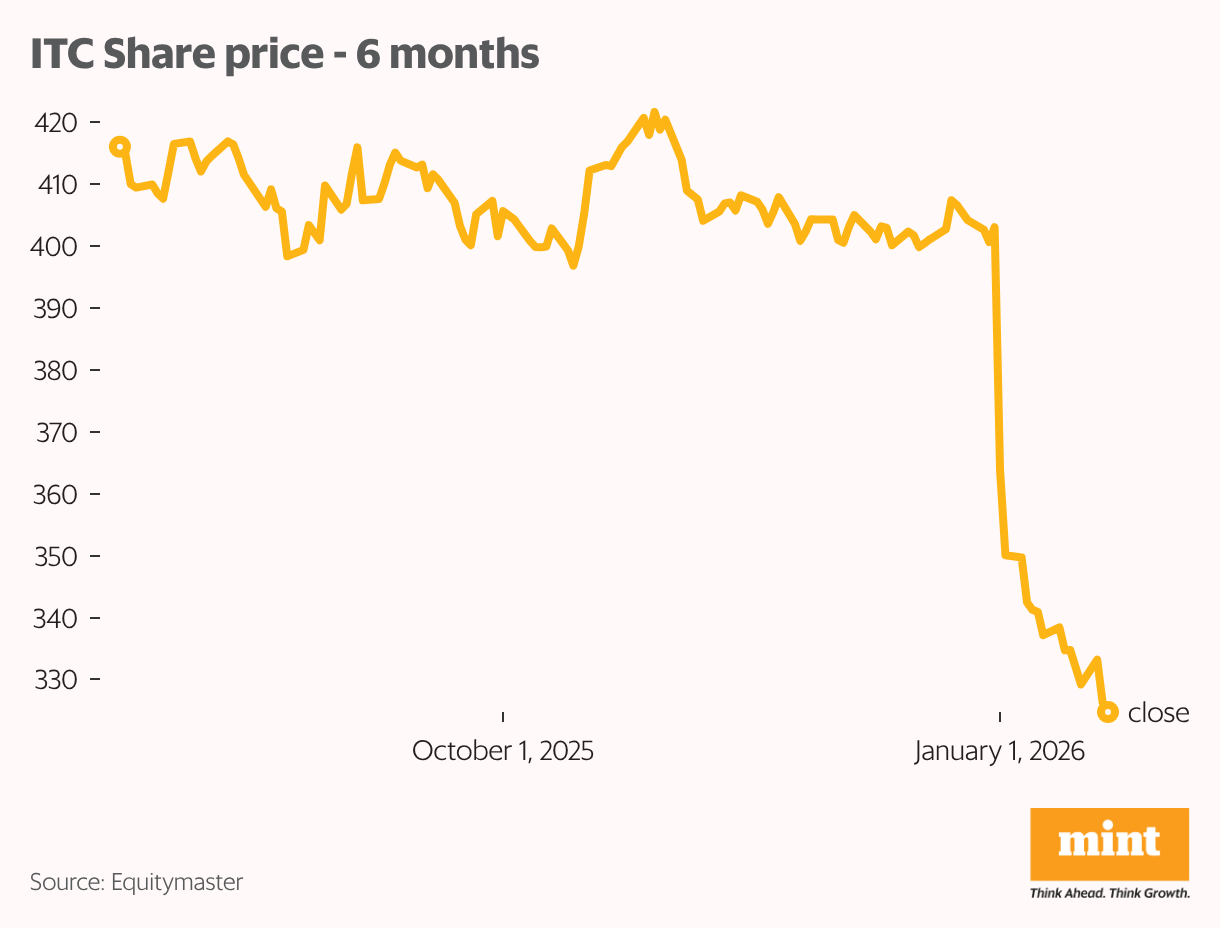

#2 ITC

ITC operates across cigarettes, FMCG, agriculture and paper-based businesses. Cigarettes remain the largest contributor, followed by FMCG and agri products.

This diversified business profile has helped ITC remain a consistent dividend payer. Even when individual businesses face cyclical pressures, the company has continued to generate cash. This has helped support dividend payouts without leaning on the balance sheet.

Q2FY26 sales declined about 4% year-on-year, largely due to a sharp 31% drop in agriculture revenue prompted by seasonality and a high base. The cigarettes business sales grew around 6.8% year-on-year, led mainly by volume and some mix improvement. Margins in the segment contracted due to elevated leaf tobacco costs, even as FMCG margins improved sequentially on stabilising commodity prices and cost initiatives.

Looking ahead, management expects the agriculture business to normalise as seasonal effects wear off, particularly since agriculture revenues were up about 7% year-on-year in the first half of the year. The company’s focus remains on the FMCG portfolio, especially premium segments and on cost discipline.

Capital expenditure requirements for the year are manageable and funded primarily through internal accruals, with no pressure on leverage.

At current levels, the stock trades at around 20.8 times earnings, which is at or below its long-term typical valuation range for the stock. Dividend yield is near 4.3%.

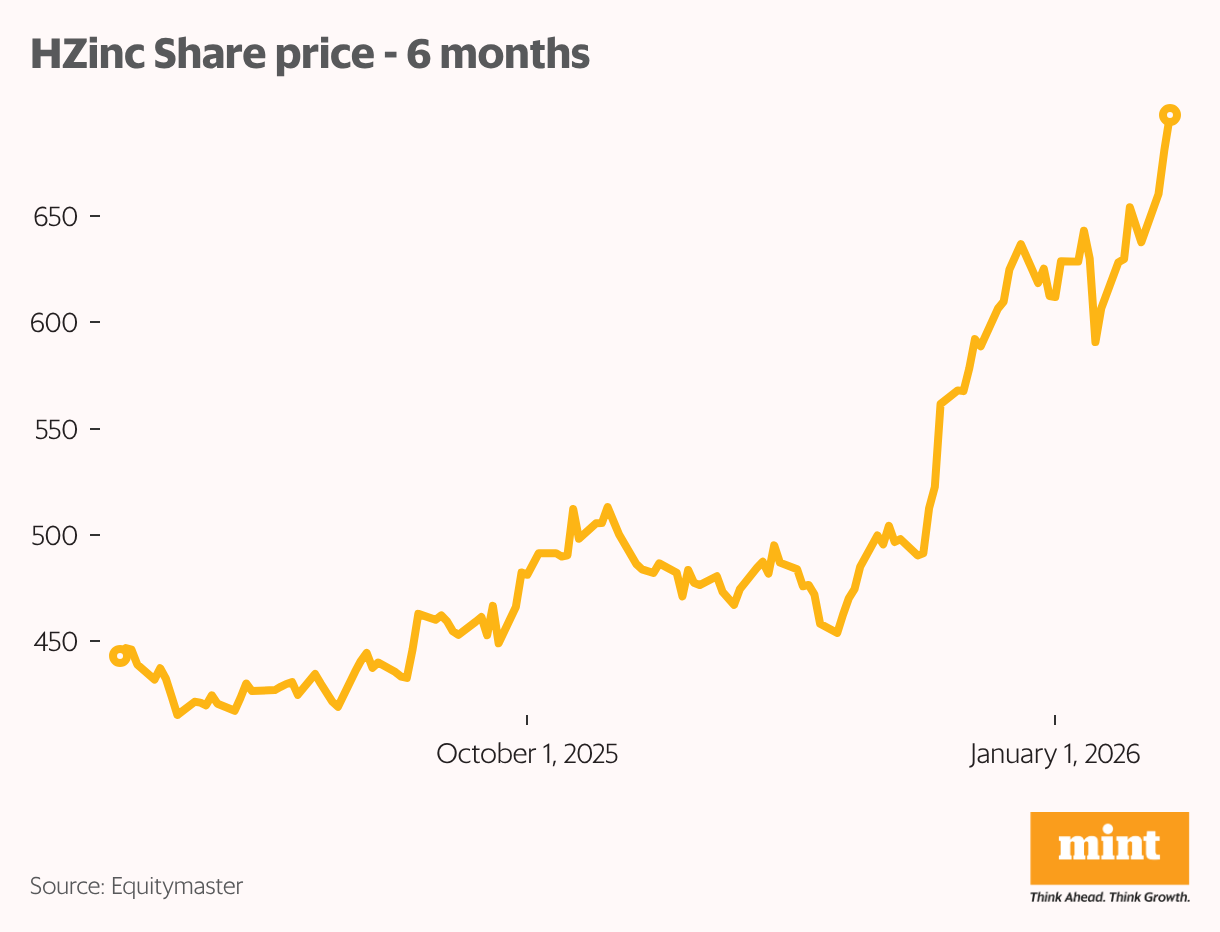

#3 Hindustan Zinc

Hindustan Zinc produces zinc, lead and silver and operates across mining and smelting. It is a business where costs, volumes and metal prices matter more than quarter-to-quarter noise. Over time, this operating structure has translated into steady cash generation.

That steady cash flow explains why the stock features among dividend stocks to watch over the next three years. Even as metal prices move through cycles, Hindustan Zinc has continued to return cash to shareholders, supported largely by operating cash flows rather than balance sheet stretch.

Q3FY26 sales grew 27% on the back of higher zinc and silver prices and improved volumes. Ebitda margins expanded during the quarter as the cost of production for zinc fell to about $940 per tonne, the lowest level in five years. Lower power costs, higher domestic coal usage and better by-product realizations kept costs in check.

Management expects this trend to continue. The zinc cost of production is guided to stay in the $950–1,000 per tonne range, which should help keep margins stable even if metal prices soften. Production across zinc, lead and silver remains on course.

Looking ahead, Hindustan Zinc will continue to invest in debottlenecking and capacity expansion across its mining and smelting operations. Any kind of capital expenditure will be focussed on improving recoveries, expanding refined metal capacity and supporting silver output. These investments are largely funded through internal accruals.

At current levels, the stock trades at around 14 times earnings, compared to a long-term median closer to 11 times.

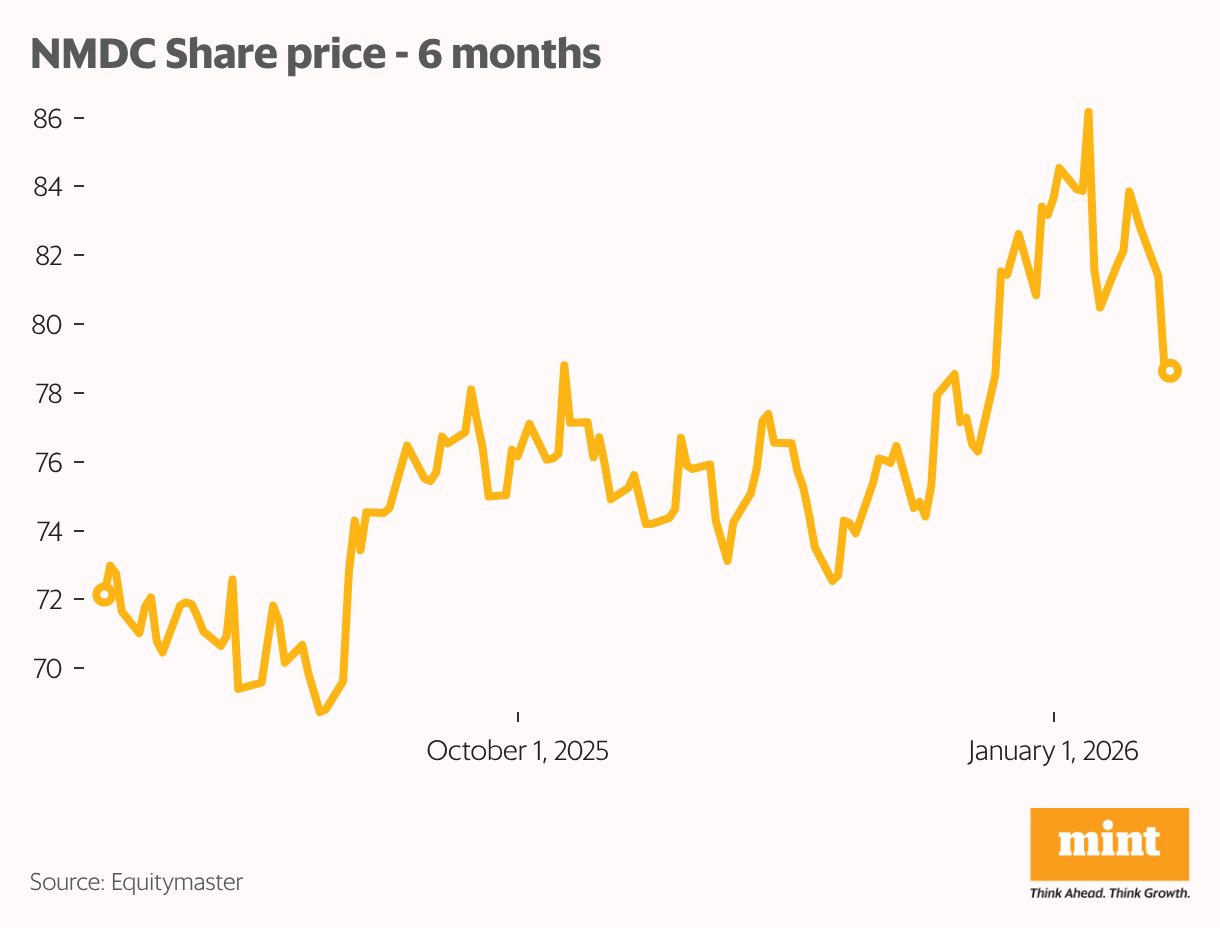

#4 NMDC

NMDC is an iron ore miner. It produces and sells lump and fines. A large part of what shows up in its numbers depends on how much it mines and what price it realises. It is a business that does not change character every few quarters.

That predictability explains why the stock features among dividend stocks to watch over the next three years. When volumes hold and costs are in check, NMDC throws up cash. A large part of that cash has found its way back to shareholders over time.

The recent quarter showed the business in a better phase. Q2FY26 sales grew 30% year-on-year, helped by higher production and better realisations. Ebitda margins remained steady at around 31%, even as royalties and levies stayed high. Operating leverage played its part, with higher volumes absorbing a part of the cost pressure.

Production and sales volumes moved up during the quarter. Iron ore production rose 23% year-on-year, while sales increased 10%.

Looking ahead, NMDC continues to focus on getting more out of its existing mines. The emphasis remains on debottlenecking, mine expansion and strengthening evacuation infrastructure.

Management has planned capex for various evacuation and capacity enhancement projects, aimed at improving the product mix and increasing production capacity to 100mt by FY29-30.

Most of this spending is expected to be funded through internal accruals. The approach reflects a preference for steady capacity building rather than aggressive expansion, with the aim of supporting volumes while keeping the balance sheet comfortable.

At current levels, the stock trades below its long-term median valuation.

#5 Power Grid

Power Grid operates the country’s interstate transmission network. It is a business built around long-gestation assets, regulated returns and steady execution. Growth here shows up gradually, as projects move from awards to commissioning.

This predictability explains why the stock features among dividend stocks to watch over the next three years. Cash flows tend to be stable, payouts have been consistent and the balance sheet is structured to absorb large capital programmes without excessive stress.

Q2FY26 capital expenditure rose sharply, up 56% year-on-year, as project awards gathered pace. Capitalisation, however, remained slow, growing 14% year-to-date. Delays related to right-of-way clearances and the shift towards tariff-based competitive bidding continued to weigh on near-term commissioning, even as the order book expanded.

Some improvement has begun to show. Capitalisation picked up from October with the start of renewable-linked substations. Management expects momentum to build through the March quarter, with around ₹8,000 crore of project starts planned. Large green corridor awards and upcoming HVDC projects have also improved visibility for growth beyond FY27.

Power Grid has emerged as a preferred bidder for a 150 MW battery energy storage project, marking its entry into grid-linked storage. The approach is to combine storage within substations rather than build standalone assets. Lower borrowing costs provide an advantage here, and management sees scope to scale this portfolio gradually as storage becomes a more regular part of the grid.

Looking ahead, Power Grid plans capital expenditure of around ₹28,000 crore in FY26, rising to about ₹35,000 crore in FY27. A large part of the spending will be towards renewable-linked transmission, HVDC corridors and select adjacencies such as storage. Funding is expected to come through a mix of internal accruals and debt, in line with the regulated asset framework.

At current levels, the stock trades close to its long-term median valuation, with dividends continuing to anchor returns.

Conclusion

Markets often feel most comfortable when prices are rising. That is usually when risks are easiest to ignore. In such phases, fundamentally strong companies provide an anchor. They may not shield portfolios from short-term swings, but they reduce the risk of lasting damage.

Dividend-paying stocks fit into this framework when payouts are supported by operating cash flows and sensible capital allocation. Dividends bring discipline and reward patience, especially in markets where price appreciation alone cannot be taken for granted.

A note of caution is still necessary. Dividends are not assured. They can be cut or deferred if business conditions change. A high yield can sometimes signal slower growth or underlying pressure rather than comfort.

This makes selectivity important. Investors need to look beyond price movements and focus on how businesses generate cash, manage leverage and invest for the future. Reading annual reports, tracking cash flow trends and insisting on a margin of safety matter more than reacting to market noise.

Over time, it is these habits that turn steady businesses into long-term wealth creators.

Happy investing.

Disclaimer: This article is for information purposes only. It is not a stock recommendation and should not be treated as such.

This article is syndicated from Equitymaster.com

Source link